A novel method to probe sparsely sampled random surfaces. Application to implied volatility modelling and prediction.

Category: Publications

A quantitative comparison of yield curve models in the MINT economies.

A semester project I supervised at EPFL comparing various econometric forecasting methods for yield curves in MINT (Mexico, Indonesia, Nigeria, Turkey) economies.

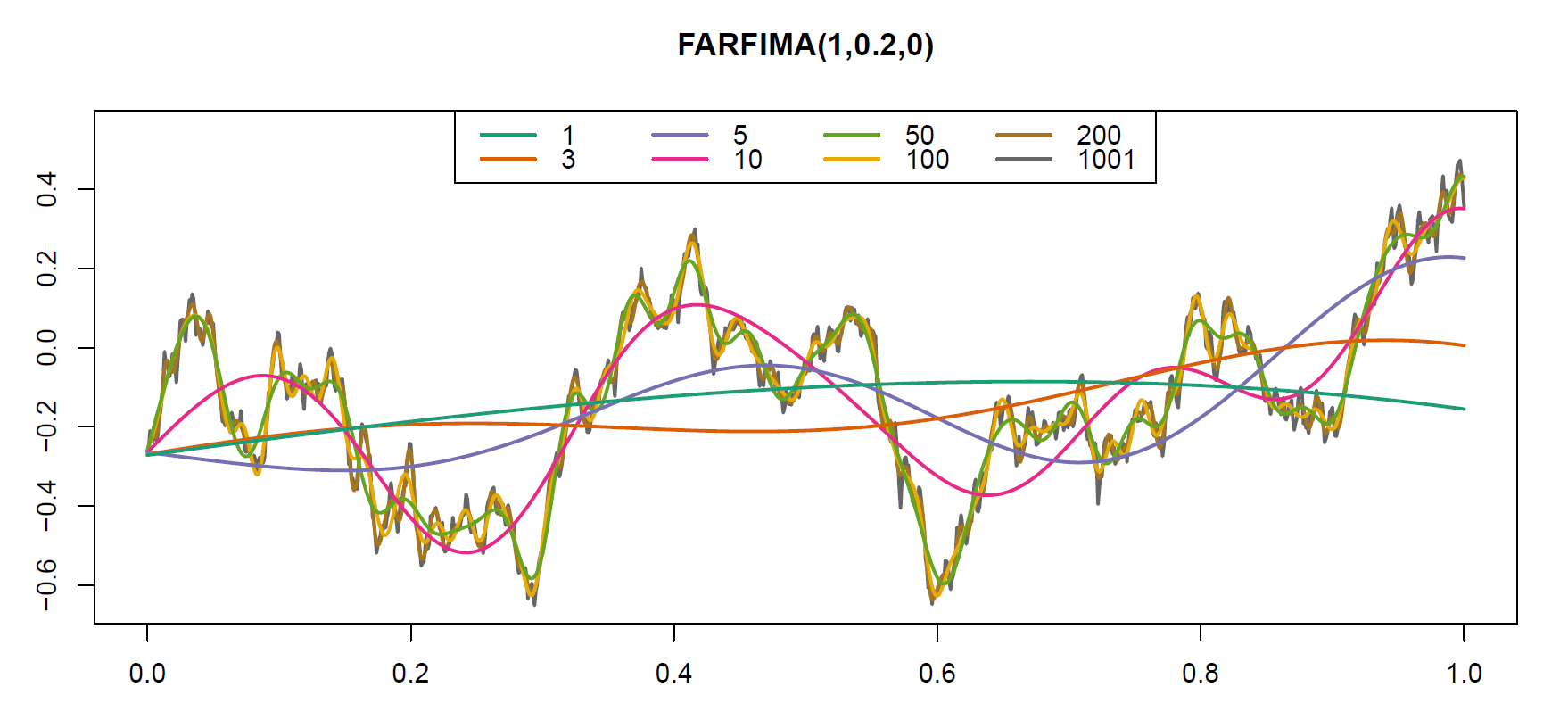

Spectral Simulation of Functional Time Series

A novel simulation method allowing for generating a wide range of simulated data, accompanied by an R package ‘specsimfts’.

Yield curve and macroeconomy interaction: evidence from the non-parametric functional lagged regression approach

In my first single-author publication I applied the tools I developed in my core PhD research to yield curve modelling.

Sparsely Observed Functional Time Series: Estimation and Prediction

The core paper of my PhD research. Published in Electronic Journal of Statistics (2020)

Functional Lagged Regression with Sparse Noisy Observations

The paper extending results from my core paper on sparsely observed functional time series. To appear in Journal of Time Series Analysis

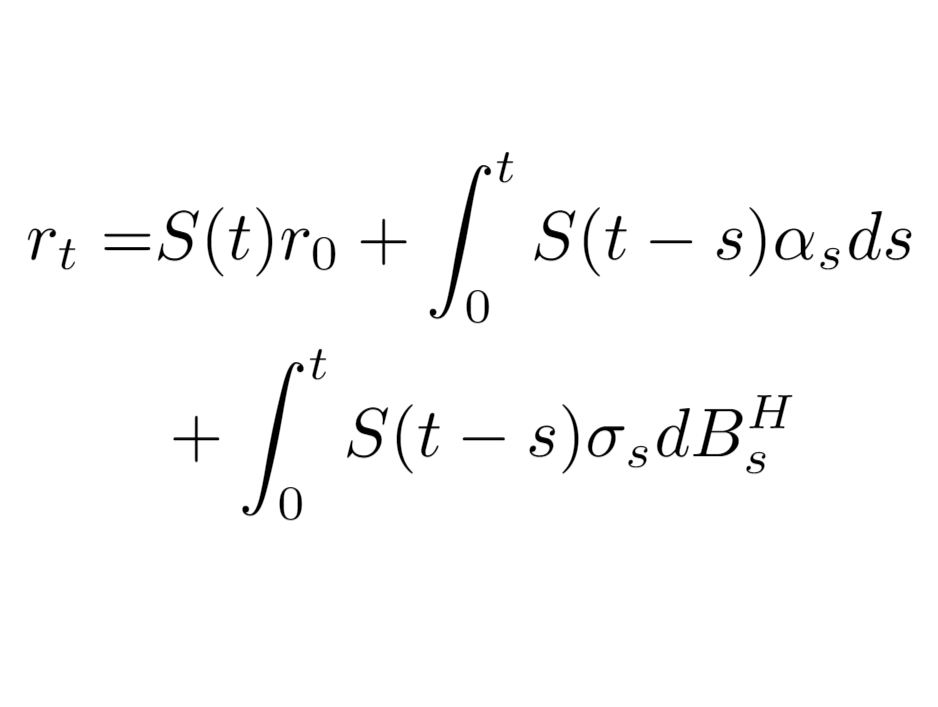

Stochastic Evolution Systems and Their Applications

My Master’s thesis in stochastic analysis (probability theory) defended at Charles University in Prague, Czechia (2016)

Fractional Brownian Motion

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

My Bachelor’s thesis in Mathematics defended at Charles University in Prague, 2013.